ATTENTION: For incorporated business owners & real estate investors with $100K+ in retained earnings

Discover How a Real Estate Investor Structured His Corporations to Pay Tax-Free Dividends to His Children

This free case study reveals the exact 3-step corporate trust structure that moved retained earnings into a tax-preferred environment and reduced the long-term tax bill — using tools Revenue Canada has already approved.

Fill out the short survey to access the case study and book your strategy call.

View our privacy policy & terms & conditions

View our privacy policy & terms & conditions

Leonard Lamarsh focuses on tax-efficient corporate planning for incorporated business owners and real estate investors with retained earnings.

What makes this different:

No cookie-cutter plans — strategy depends on your corporation and ownership structure

Focus on reducing long-term tax exposure on corporate surplus

Works alongside your accountant and legal team

Most incorporated business owners unknowingly carry one or more of these structural problems inside their corporation

The Tax Trap on Surplus

Retained earnings sit inside the corporation year after year. Taking them out as salary or dividends triggers a large personal tax bill. Leaving them in exposes the estate to a significant tax hit on death.

No Succession Structure

Many investors want to involve their children in the business, but have no legal ownership structure in place. The wealth stays concentrated in the founder until death, then faces probate and estate tax.

No Protection if You Stop Working

If a critical illness or accident stops you from working, the corporation has no mechanism to cover debt, operations, or lost income. The portfolio is exposed at exactly the moment you are least able to manage it.

Are You Extracting Income from Your Corporation in the Most Tax-Efficient Way?

Many incorporated investors pay significant dividend tax year after year — not because they lack advisors, but because their corporate structure was never designed to optimize how retained earnings are extracted. Even modest structural changes can significantly improve how corporate profits convert into personal and family wealth, while preserving long-term growth capacity.

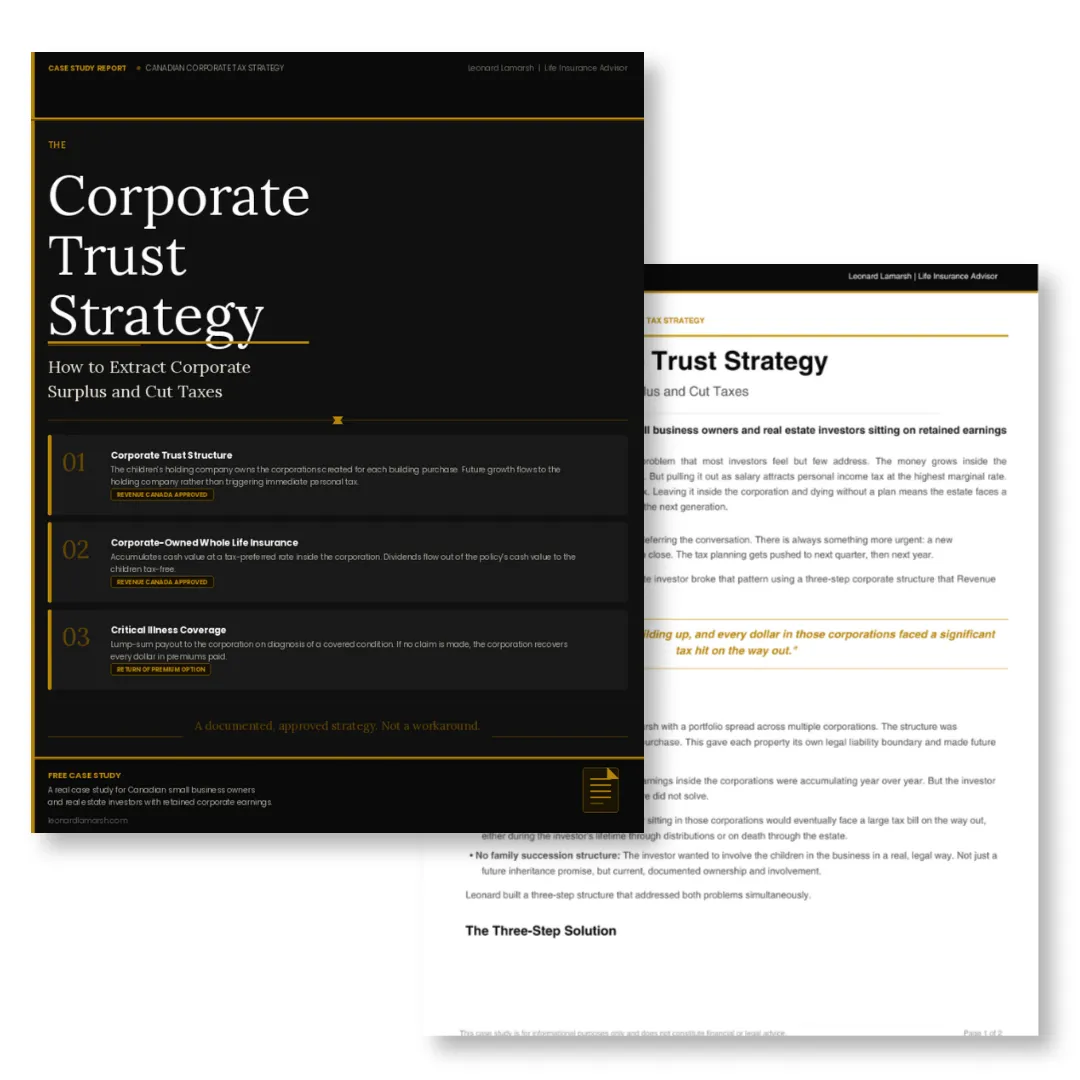

The Real Estate Investor Who Built a Tax-Free Dividend Structure for His Children

A real estate investor came to Leonard with a portfolio spread across multiple corporations, one per building purchase. The retained earnings were accumulating fast. Every dollar faced a heavy tax bill on the way out. The investor also wanted his children genuinely involved in the business, not just as future heirs.

Leonard designed a three-step structure. The children's holding company now owns the corporations created for each building. A corporate-owned whole life insurance policy accumulates cash value at a tax-preferred rate inside the corporation. When dividends are paid to the children, that money flows from the policy's cash value — tax-free. Revenue Canada has approved this mechanism. A corporate-owned critical illness policy with a return of premium option was also added: full protection if something goes wrong, and premiums returned to the corporation if nothing does.

Before the Structure

Retained earnings growing with no exit strategy

Every dividend distribution triggered personal tax

Children had no legal ownership stake

No protection if the investor stopped working

Estate exposed to full tax bill on death

After the Structure

Surplus moved into a tax-preferred environment

Dividends paid to children tax-free from policy cash value

Children hold documented ownership via holding company

Critical illness coverage protects the portfolio

Estate tax exposure reduced significantly

Is Your Corporate Wealth Properly Protected

Against Risk?

Operating companies accumulate value, but they also carry risk. Without the right structure, retained earnings remain exposed to business liabilities, creditor claims, and — most commonly — the personal health and mortality of the owner. Strategic structuring separates growth from risk and protects what you have already built.

The Couple Who Needed $750,000 in Mortgage Insurance and Waited Six Months Too Long

An older couple came to Leonard needing $750,000 in mortgage insurance. It was a straightforward need. The product existed. The process was simple. They said they would think about it and come back.

Six months later they returned. In that time, the husband's age had moved him out of the eligibility window for a standard Term 20 policy. The coverage they needed — the coverage that would have been routine six months earlier — was no longer available at standard rates. They ended up in a financial crisis.

The strategy was not complicated. The delay was the entire problem. Insurance eligibility is not just about health. Age is a hard cutoff. Every month of delay narrows your options. Products available today at standard rates may require rated premiums or become unavailable entirely based on what changes in your age bracket. There is no recovering from a missed window.

Is Your Exit and Legacy Plan Optimized for Maximum After-Tax Wealth Transfer?

At sale, transfer, or death, a substantial portion of a corporation's value can be eroded by capital gains tax, probate costs, and inefficient estate structuring. Many owners discover too late that their succession planning was incomplete or never integrated with their corporate strategy. The difference between a basic plan and an optimized one can represent hundreds of thousands of dollars preserved for the next generation.

The Client Who Bought a Life Insurance Policy for a Child 15 Days Old

One client came to Leonard not because of a tax crisis, but because of a long view. They wanted to build financial assets for their children from the earliest possible date, and they wanted to use it as a tool to teach those children about compound growth, patience, and long-term thinking.

Leonard helped them purchase a whole life insurance policy for the child when the baby was 15 days old. The goal was not morbid planning. The goal was compound interest. A policy started at 15 days old has decades to accumulate cash value before the child reaches adulthood. By the time that child is ready to fund education, start a business, or make a first property purchase, the policy has built real, accessible value.

For investors with retained corporate earnings, a policy like this can be funded at the corporate level using the same approved structures described in the case study above. The premiums come from pre-tax corporate dollars rather than after-tax personal income, which reduces the effective cost significantly.

15

Days old when policy started

Tax-Free

Cash value accessible in adulthood

Corporate

Funded with pre-tax dollars

This is not a sales presentation

It is a structured 30-minute review designed for Canadian incorporated business owners and real estate investors with meaningful retained earnings who want clarity on how their corporate structure is positioned — today and long-term.

Leonard reviews your situation before the call so the conversation is focused from the first minute. You do not need to prepare anything. If a structure like the ones described above makes sense for your situation, he will walk you through what next steps look like. If it does not, he will tell you that too and point you in the right direction.

Your Advisor

Leonard Lamarsh

Life Insurance Advisor | Canadian Corporate Strategy

Leonard Lamarsh works with Canadian small business owners and real estate investors who have retained earnings inside their corporations and no clear plan for what to do with them. His focus is on structures that are already approved by Revenue Canada and that work in parallel with a client's existing operations — not instead of them.

The cases in this report are real. The investors involved were busy people running real businesses, who kept putting off the conversation until they found a thirty-minute window to have it. Leonard's role is to make that thirty minutes as useful as possible.

He works alongside your CPA and legal advisors, not in place of them. His job is the insurance and structuring layer that most generalist advisors do not specialize in.

Your Corporation Is Growing.

The Tax Bill Is Growing With It.

The structures in this case study are approved, documented, and in active use by Canadian investors today. The only difference between them and investors who have not acted yet is timing. Book your free 30-minute second opinion call now.

CONTACT US

Give us a call, send us an email, or visit our office!

Phone: (780) 905-2580

Email: [email protected]

Address: 10612 29 Ave NW #204, Edmonton Alberta T6J 4H6

Copyright 2026 | Gold Capital Financial Services